Wealth Transfer Information (inheritance sales) for Real Estate Professionals

Wealth Transfer Information (inheritance sales) for Real Estate Professionals

Up until this section this handbook has provided information to position you as a subject matter resource (not expert) in scenarios involving senior life decisions. This sections summarizes key concepts of how wealth – including real estate – is passed from one generation to another.

The passing of wealth in many cases results in a real estate sales transaction by those that inherit a home (or homes) and as mandated by a judge if the estate goes to probate with no valid trust or will. If an agent providing value as a subject matter resource can help motivate a senior to set up the most efficient way to transfer an estate (homes included) under the supervision of a professional in the field to the persons(s) the senior wishes to inherit their assets, the resulting benefits to the seniors, those that would inherit the estate and the agent can be huge. Listen to the podcasts with Bevin Eustace, Amanda Wheeler and Betty Kerr if you want to learn what can happen without a trust or valid will.

Keep in mind that proceeds from an estate sale of a home and other assets make great down payments on subsequent homes purchased by the heirs. An eighty five year old senior leaving a $600k home to three heirs by setting up a trust can result in one to four home sales – the trustee sale itself and three possible $200k down payments for three additional home purchases.

While always positioning yourself as a resource and not an expert, try to determine if a trust exists and if it is updated. Encourage your clients to update their trusts with a professional in the field. If they have no trust, recommend that they explore the advantages of a trust with a licensed professional. It’s possible a trust (1) saves money vs. probate, (2) saves time vs. probate, and (3) may create a listing in a matter of weeks vs months/years with an estate going through probate. Always advise your seniors to consult a professional and never speak in terms that can be construed as legal advice.

What is a will?

Your will is a legal document in which you give certain instructions to be carried out after your death. For example, you may direct the distribution of your assets (your money and property), and give your choice of guardians for your children. It becomes irrevocable when you die. In your will, you can name:

Your beneficiaries. You may name beneficiaries (family members, friends, spouse, domestic partner or charitable organizations, for example) to receive your assets according to the instructions in your will. You may list specific gifts, such as jewelry or a certain sum of money, to certain beneficiaries, and you should direct what should be done with all remaining assets (any assets that your will does not dispose of by specific gift).

A guardian for your minor children. You may nominate a person to be responsible for your child’s personal care if you and your child’s other parent die before the child turns 18. You may also name a guardian — who may or may not be the same person — to be responsible for managing any assets given to the child, until he or she is 18 years old. You can also nominate a guardian in a separate writing other than a will. Such a writing should be signed by all of the child’s parents.

An executor. You may nominate a person or institution to collect and manage your assets, pay any debts, expenses and taxes that might be due, and then, with the court’s approval, distribute your assets to your beneficiaries according to the instructions in your will. Your executor serves a very important role and has significant responsibilities. It can be a time-consuming job. You should choose your executor carefully. An executor is entitled to compensation for the services provided.

Keep in mind that a will is just part of the estate planning process. Whether your estate is large or small, you probably need an estate plan.

What happens if I don’t have a will?

If you die without a will (referred to as intestate), California law will determine the beneficiaries of your estate. Contrary to popular myth, if you die without a will, everything does not automatically go to the state. If you are married or have established a registered domestic partnership, your spouse or domestic partner will receive all of your community property assets. Your spouse or domestic partner also will receive part of your separate property assets, and the rest of your separate property assets will be distributed to your children or grandchildren, parents, sisters, brothers, nieces, nephews or other close relatives.

If you are not married or in a registered domestic partnership, your assets will be distributed to your children or grandchildren, if you have any — or to your parents, sisters, brothers, nieces, nephews or other relatives. If your spouse or domestic partner dies before you, his or her relatives may also be entitled to some or all of your estate. Friends, a non-registered domestic partner or your favorite charities will receive nothing if you die without a will. The State of California is the beneficiary of your estate if you die intestate and you (and your deceased spouse or domestic partner) have no living relatives.

What is Probate?

Probate means that there is a court case that deals with: • Transferring the property of someone who has died to the heirs or beneficiaries; • Deciding if a will is valid; and • Taking care of the financial responsibilities of the person who died. In a probate case, an executor (if there is a will) or an administrator (if there is no will) is appointed by the court as personal representative to collect the assets, pay the debts and expenses, and then distribute the remainder of the estate to the beneficiaries (those who have the legal right to inherit), all under the supervision of the court. The entire case can take between 9 months to 1 ½ years, maybe even longer.

If you have the legal right to inherit personal property, like money in a bank account or stocks, and the estate is worth $150,000 or less, you may NOT have to go to court. There is a simplified process you can use to transfer the property to your name. The value of the property is based on what it was worth on the date of death —not on what the property is worth now.

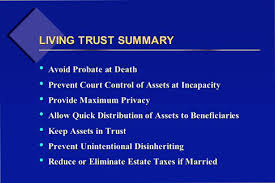

- Keep in mind, this process CANNOT be used for real property, like a house. If the person left $150,000 or less in real property, including some personal property, you may be able to use a form called Petition to Determine Succession to Real Property (Estates $150,000 or Less) (Form DE-310). You will have to file the Petition with the court, obtain and file an Inventory and Appraisal (Form DE-160), and provide notice of hearing. Talk to a lawyer to make sure you can use this simplified process in your case. A living trust is a legal document created by you (the grantor) during your lifetime. Just like a will, a living trust spells out exactly what your desires are with regard to your assets, your dependents, and your heirs. The big difference is that a will becomes effective only after you die and your will has been entered into probate. A living trust bypasses the costly and time-consuming process of probate, enabling your successor trustee (who fills basically the same role as an executor of a will) to carry out your instructions as documented in your living trust at your death, and also if you’re unable to manage your financial, healthcare, and legal affairs due to incapacity.

The two types of living trusts:

- Revocable living trust: With a revocable living trust, you transfer your assets into the ownership of the trust. You retain control of those assets as the trustee of your revocable living trust. You can change or revoke the trust at any time you want. The assets in the trust pass directly to your beneficiaries without going through probate upon your death. However, neither wills nor revocable living trusts avoid or minimize estate taxes.

- Irrevocable living trust: An irrevocable trust allows you to permanently and irrevocably give away your assets during your lifetime. After you give away these assets, you have relinquished all control and interest in these assets. Due to that fact, these assets are no longer considered part of your estate and aren’t subject to estate taxes. As you likely imagine, an irrevocable trust is appropriate in only extremely rare circumstances, such as when you have more money than you or your spouse could ever use. Your beneficiaries would benefit at Uncle Sam’s expense if you utilized an irrevocable trust to reduce your taxable estate before your death.

- Living trusts (revocable or irrevocable) typically cost $1,000 to $3,000 per person.

Should everyone have a living trust?

No. Whether or not to create a trust is a personal decision. Young married couples without significant assets and without children, who intend to leave their assets to each other when the first one of them dies do not necessarily need a living trust. However, if the couple should die in a common accident, or shortly after each other, without a trust their estate(s) may be subject to a probate. Other persons who do not have significant assets (less than $150,000) and have very simple estate plans also do not need a living trust. Finally, anyone who believes that court supervision over the administration of his or her estate would be beneficial should not have a living trust. The greater the value of your assets (particularly if you own real estate), the greater the benefits of a living trust. Having a living trust could be important in the event of an accident or sudden illness.

Who needs estate planning?

You do — whether your estate is large or small. Either way, you should designate someone to manage your assets and make health care and personal care decisions for you if you ever become unable to do so for yourself. For many, such “life planning” is the most important aspect of an estate plan.

If your estate is small, your plan may simply focus on who will receive your assets after your death, and who should manage your estate, pay your last debts and handle the distribution of your assets. If your estate is large, your lawyer will also discuss various ways of preserving your assets for your beneficiaries and of reducing or postponing the amount of taxes which otherwise might be payable after your death.

If you fail to plan ahead, a judge will appoint someone to handle your assets and personal care. And your assets will be distributed to your heirs according to a set of rules known as intestate succession. Contrary to popular myth, everything does not automatically go to the state if you die without a will. Your relatives, no matter how remote, and, in some cases, the relatives of your spouse, have priority in inheritance ahead of the state. Still, they may not be your choice of heirs; an estate plan gives you much greater control over who will inherit your assets after your death.

Who can I call with questions or if a Senior I’m working with has questions?

Law Offices of Amanda G. Wheeler